Nobody wants to run out of money in retirement. I’ve worked with retirees who have, and I can attest that it’s not a fun situation to be in. We’ll explain a unique and little-known “retirement insurance” strategy that can help protect and preserve your retirement nest egg for longer.

Table of Contents

Does Your Financial Plan Include “Retirement Insurance”?

Imagine being in your late 80s, in declining health, and you’ve just run out of money. Your retirement account, your checking account, your savings account – all dry.

To add insult to injury, your A/C unit just died and it’s 95 degrees and humid as a swamp outside. It costs $7,000 to replace your A/C . . .

. . . but you’re dead broke.

Sadly, I’ve worked with people in situations like this, and it’s not a fun place to be.

Unfortunately, in my experience, retirees often follow the conventional wisdom and only call for help after they’ve already run out of money. A better strategy is to get help before you run out of money.

Even better, you want to protect yourself ahead of time so you hopefully don’t run out of money in the first place. That’s what this unique and little-known “retirement insurance” strategy is all about.

To be clear, there’s no insurance product called “retirement insurance”. We’re not trying to sell you an insurance policy here.

The term “retirement insurance” refers to a strategy that takes advantage of the equity in your home to help reduce the risk of draining your retirement assets faster than planned.

The financial tool that can accomplish this is called a home equity conversion mortgage, or HECM. The FHA-insured HECM is the most common reverse mortgage product in the United States today.

Now before you close your web browser and run away screaming, please hear me out. Like annuities, reverse mortgages have gotten a bad rap over the years. They’re not what they used to be.

Contrary to popular belief, a reverse mortgage is not for broke and desperate people. It’s not just a loan of last resort for those who have no other options. Frankly, the broke and desperate often don’t qualify.

Today, the best candidates are those who are at least reasonably financially stable. The best strategy is to use a reverse mortgage as a safety net to help your retirement nest egg last longer.

Hang with me and I’ll show you how this strategy can profoundly increase the longevity of your retirement assets, lifestyle, and financial security.

A Safety Net, Not a Lifeboat

Many very smart people still think a reverse mortgage is a loan of last resort just for broke and desperate people. Commentators and pundits commonly say that you should wait as long as possible and only get a reverse mortgage when you really need it.

Unfortunately, this kind of advice is rampant, and many retired homeowners end up following it – with disastrous results.

Check out the following from an article over at Housing Wire:

“. . . we still have advisors out there who, without a shred of evidence, are telling retirees to use a reverse mortgage only as a last resort, even though academics have demonstrated over and over that’s the worst way to use it,” [Longevity View Associates Principal Shelley Giordano] said.

“When you use the HECM as a last resort, your cash flow and your portfolio have already been depleted,” Giordano said. “This is a pretty huge hole, so retirement income experts suggest the coordination of housing wealth with other assets throughout retirement in order to help protect against catastrophes.” (emphasis mine)

Source: https://www.housingwire.com/articles/46370-the-funding-longevity-task-force-wants-you-to-know-about-reverse-mortgages

In other words, a retiree who waits as long as possible to get a reverse mortgage may already be beyond help. The financial hole may be too large for a reverse mortgage to plug.

The better strategy is to use home equity “in coordination” with your other retirement assets to prevent a financial catastrophe in the first place.

Wade Pfau, a prominent retirement researcher and thought-leader in the reverse mortgage space, writes:

[The reverse mortgage] must not be viewed in isolation, but rather as how it contributes to an overall plan. The value of the reverse mortgage can mostly be found in its diversifying benefits for investments in retirement. Taking distributions from investments can dig a hole that is hard to recover from, and wise use of the reverse mortgage protects the investment portfolio in retirement.

Source: https://www.advisorperspectives.com/articles/2019/04/15/what-the-critics-get-wrong-about-reverse-mortgages

Life can throw a variety of financial curveballs at you: bad stock market, medical bills, long-term care expenses, home repairs and maintenance, family members needing money, etc.

If you want your money to last at least as long as you do, you need to have as many financial options as possible. The reverse mortgage strengthens and diversifies your assets by adding an additional cash source to the picture: home equity.

Now, before I demonstrate how a reverse mortgage can strengthen your retirement plan, let’s first cover a few basics about how a reverse mortgage works.

How a HECM Works

If you’re at least 62, a HECM reverse mortgage enables you to convert home equity into cash with no mortgage payments and without giving up ownership of your home.

No mortgage payments are required as long as at least one borrower (or non-borrowing spouse) lives in the home, maintains it, and pays the required property charges.

You remain the owner of your home and you’re free to leave it to your heirs. Your heirs will inherit any equity remaining in your home.

The HECM is a non-recourse loan; the most that will ever have to be repaid is the value of your home. If your home isn’t worth enough to pay off the entire balance, FHA will cover the shortage.

The HECM is a mortgage, so it has an interest rate like any other mortgage. Rates are typically comparable to traditional “forward” 30-year mortgage rates.

The reverse mortgage is highly versatile, which means it can be fine-tuned to achieve your individual goals and needs. Proceeds can be received as term or tenure income, line of credit, lump sum, or some combination of all of these options.

The line of credit option is what I will focus on for our “retirement insurance” strategy. It’s ideal for several reasons:

- No monthly payments are required. You don’t need to worry payments eating up your monthly cash flow when you withdraw funds.

- You can rely on it. As long as you remain in good standing, your available credit cannot be locked, chopped, frozen, or taken away. FHA guarantees the funds even if your lender goes out of business.

- The available credit grows. The line of credit is designed to grow and compound larger over time, giving you access to more equity if you need it. There’s no limit on how much the available credit can grow.

Now that we’ve covered the basics, I want to demonstrate how a reverse mortgage line of credit can help protect and preserve your retirement assets for longer.

The HECM as “Retirement Insurance”

To see how a reverse mortgage line of credit can serve as “retirement insurance”, let’s check out a case study.

First, let’s assume it’s January 1, 2007 and two 65-year old bachelors named Nolan and Harry have just retired.

I am setting this scenario in 2007 because I want to show you how the HECM line of credit can preserve retirement assets through a bad bear market. I will use real-world stock market data (courtesy of Yahoo! Finance) for the illustration.

Let’s also assume Nolan and Harry have the exact same financial profile: they each own free and clear homes worth $300,000 and have non-taxable Roth IRAs worth $250,000.

On January 1, 2007, they both move 100% of their IRAs into VSCGX (note that this is not investment advice nor an endorsement of this fund), a conservative balanced fund trading at $16.73. With their $250,000, they are able to purchase 15,000 shares each.

Both men plan to supplement their Social Security income with $1,000/month from their retirement accounts.

Before we dig into this further, let’s review our starting assumptions for both retirees:

- Age: 65

- Home value: $300,000

- Mortgage balance: $0

- Roth IRA: $250,000 invested in 15,000 shares of VSCGX

- Planned monthly retirement account withdrawal: $1000

Nolan and Harry happen to use the same accountant, who’s name is Joe. Joe is concerned that the stock market is about to go down, so he recommends that both men set up a reverse mortgage line of credit to supplement their Social Security and Roth IRAs.

Harry agrees with Joe and immediately gets a reverse mortgage line of credit. His available credit starts off at $121,700 and has an annual growth rate of 5.87%.

Harry also decides to leave his IRA untouched and instead take $1,000/month from the line of credit starting in January 2007. He figures he’ll leave the IRA alone until the stock market improves. He doesn’t want to sell shares into a falling market because it increases the risk he’ll drain his IRA dry sooner than planned.

Nolan, on the other hand, says “Bah! I don’t need no stinkin’ reverse mortgage! I’m not broke and desperate and I’m not going to let the bank steal my house!”.

Of course, Nolan’s worries about the bank stealing his house are unfounded, but he can’t be convinced otherwise. He figures he’s got plenty of money, so he’ll live on his Social Security and the $1,000/month from his IRA regardless of what happens with the stock market.

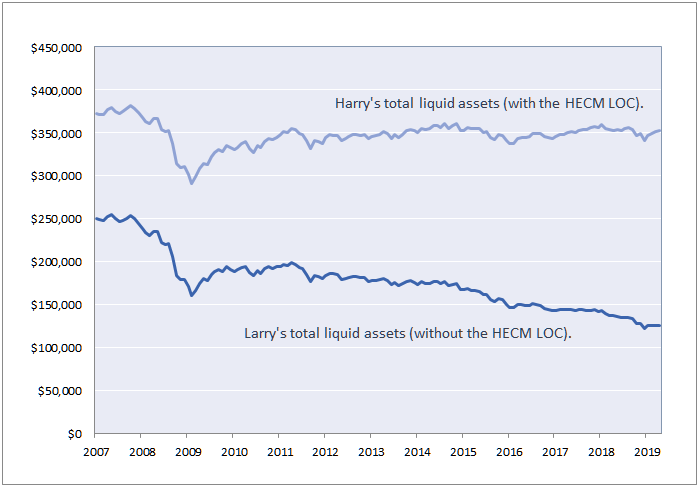

Fast forward to 2019

Let’s fast forward twelve years to 2019 and see how Nolan and Harry end up.

Remember, Nolan chose not to get a reverse mortgage back in 2007. He figured he would ride out the stock market come hell or high water. He has faithfully withdrawn $1000/month from his IRA every month since he retired – even through the terrible bear market years of 2008 and 2009.

Nolan’s IRA is now worth around $126,000, which means he’s burned through almost half the value of his portfolio in just 12 years! Yikes!

Even more alarming, Nolan has only 6,315 shares left of the original 15,000 he had when he retired. He’s burned through almost two thirds of his shares.

The share price of VSCGX dropped badly in 2008 and 2009, which forced Nolan to sell more shares to maintain his $1,000/month income requirements. When he retired, he only needed to sell 60 shares to get $1,000. At the market bottom in 2009, he had to sell 80 shares to get the same income.

Nolan now has just a little more than 1/3 of his shares left, yet he could potentially live another 10 or 20 years. Nolan is in danger of running out of money.

Harry, on the other hand, left his IRA untouched through the bear market in 2008 and 2009. It was painful to watch the IRA go down in value, but it recovered completely by early 2011.

In February 2011, Harry decided to stop his withdrawals from the reverse mortgage line of credit in favor of withdrawals from his Roth IRA. His IRA was performing well, so it made sense to live on that instead.

So, how do Nolan and Harry stack up today? Which one had the better strategy? Well, I think the graph below speaks for itself.

As you can see, both men took a hit in 2008 and 2009. However, Harry’s portfolio (the top line) is in much better shape than Nolan’s portfolio (the bottom line).

Nolan’s portfolio took a beating during the Great Recession and never recovered. It continues to dwindle fast despite the strong bull market since the 2009 bottom.

Harry took a hit, too, but his total liquid assets have recovered nicely. Because he was able to pick and choose which asset to withdraw from based on market conditions, he was able to more effectively preserve his overall portfolio.

Even though Harry consistently pulled out $1,000/month, his total liquid assets are just a little less than what he had when he retired twelve years ago.

Nolan, on the other hand, has seen his liquid assets drop by almost half.

Folks, it’s pretty obvious who has the more financially secure retirement. Harry chose to use a HECM line of credit as “retirement insurance”. Nolan did not, and I think the results speak for themselves.

Preserving Your Assets For Longer

Hopefully you can see the value of adding a reverse mortgage line of credit to the retirement planning picture. Retirement can last potentially 20 or 30 years. It’s essential to have as many financial resources available as possible.

How many more times will you have to replace the roof on your house? Will you need to replace your car at some point? What if you get hit with medical bills? What if the stock market goes down? What if you need long-term care?

Again, you want to have as many financial resources available as possible.

As we’ve covered, the reverse mortgage is not a loan of last resort for the broke and desperate. It’s best used as part of a broader retirement plan. When you use it strategically as part of a retirement plan, it serves as “retirement insurance”, which helps protect and preserve your retirement assets, lifestyle, and financial security for longer.

Additional Resources

Robert Powell of TheStreet’s Retirement Daily sat down with Steve Resch, Vice President – Retirement Strategies at Finance of America, for an interview that covered a few different topics, but emphasized how a reverse mortgage can increase financial security in retirement.

The interview is worth your time and can be found here.